Is your business ready for the biggest tax change since PAYE?

![]() Making Tax Digital for Business (MTDfB) is undoubtedly the biggest change to the administration of tax since the introduction of PAYE in the first half of the last century. It will affect every business in the UK with turnover in excess of the VAT registration threshold, in particular, changing the way that businesses keep their accounting records and report their profit to HMRC.

Making Tax Digital for Business (MTDfB) is undoubtedly the biggest change to the administration of tax since the introduction of PAYE in the first half of the last century. It will affect every business in the UK with turnover in excess of the VAT registration threshold, in particular, changing the way that businesses keep their accounting records and report their profit to HMRC.

MHA MacIntyre Hudson explains the latest requirements of the MTDfB regime and what you need to do now to prepare your business for the changes.

The original proposals

MTDfB was originally designed for income tax purposes. This meant that from April 2018, the self-employed and landlords would have to:

- Keep digital accounting records. They would be able to continue to use spreadsheets for record keeping, but had to ensure that the spreadsheet met the necessary requirements of MTD. This would involve combining the spreadsheet with software.

- Update HMRC with their summary income and expenses at least quarterly with software that complies with MTD

- Finalise the annual accounts and tax computation and submit them to HMRC within ten months of the end of the accounting period.

It was also going to be possible for businesses to opt into a pay as you go system for the collective payment of taxes.

The latest

Chris Barlow, MHA MacIntyre Hudson

The Government has revised its timetable for MTDfB. Under the latest plans:

- Only businesses with a turnover above the VAT registration threshold will have to keep digital records

- They will need to do so from April 2019 for VAT reporting

- For income tax reporting obligations, the self-employed and landlords will not be asked to keep digital records or to update HMRC quarterly, until at least 2020

- There are no changes from the original proposal for companies.

Exemptions

The exemptions that already apply to electronic VAT returns will be extended to cover digital record keeping requirements. They include:

- Practising members of a religious society or order whose beliefs are incompatible with the use of electronic communications

- Insolvent businesses

- Businesses for whom online filing is not reasonably practicable for reasons of disability, age, remoteness of location, or any other reason.

If a charity is registered for VAT it will fall under the MTD for VAT regime on 1 April 2019.

Why else should I go Digital?

The increasingly entrepreneurial and competitive business environment has created a need for businesses of all sizes to have more frequently updated financial information, through the use of cloud based accounting software. If a business doesn’t strike on opportunities while the iron is hot, they miss out. The ability to move quickly very often depends on the financial position of the business, but looking at the prior year’s accounts doesn’t necessarily shed light on the current position.

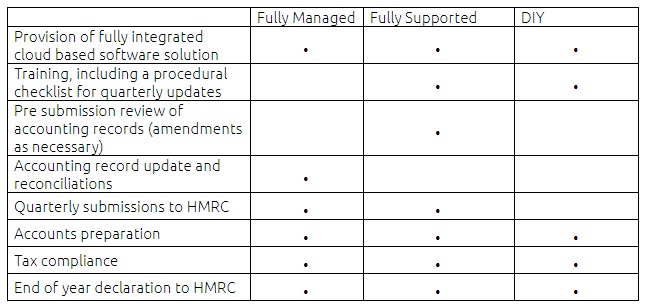

Our services

We offer a range of services and support to assist you with meeting your obligations under MTDfB. Whether you simply need advice on software or you are looking for us to take the burden of quarterly reporting off your hands entirely, we have a package to cater for your needs.

Contact us

For advice on implementing digital systems or for further information on what MTDfB means for you, please contact Chris Barlow on 0121 236 0465 or email chris.barlow@mhllp.co.uk