“Lower carbon investing in challenging market conditions”

Rupert Edwards, Specialist Environmental Adviser

It has been a very challenging year for ethically oriented investors not only in financial terms but also in relation to achieving low carbon or other ESG (environmental, social and corporate governance) goals.

Institutional investors, such as pension funds, have been increasingly focused on the transition to net zero greenhouse gas emissions.

For example, the UN convened Net-Zero Asset Owner Alliance, representing 74 institutional investors with $10.6 trillion in assets under management, is aiming to transition to net zero investment portfolios by 2050.1

This is consistent with the Paris Agreement’s Article 2.1(c) which describes “making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.”2

Many private investors want their savings aligned with this transition and some may be willing to go further to achieve net zero before 2050.

However, efforts by investment managers and other financial institutions to decarbonise portfolios are hamstrung by their inability to exercise direct control over the emissions of companies to which they provide finance.

Financial institutions can engage with companies and advocate for regulatory changes to push for progress on low carbon goals.

And the Science-Based Target Initiative (SBTi) is developing standards that allow for evaluation of pledges by

corporates and financial institutions to reach net zero.3

However, the fiduciary responsibility to maximise returns means that institutional investors inevitably struggle to decarbonise investments beyond a level implied by the efforts of public policy and the real economy, without risking lower financial returns.

Constructing net zero portfolios by tilting towards low-emitters and those best-in-class carbon-intensive companies transitioning to net zero has been easier said than done.

From 2016 through 2020, MSCI found that less than a quarter of MSCI ACWI Investable Markets Index (IMI) constituents decarbonised by at least 10% per year, making it virtually impossible to build broad global equity portfolios of decarbonising companies during this period.

ESG funds (as opposed to low carbon funds) have faced a barrage of criticism in recent months, from the mild: that the acronym ESG jams together disparate and sometimes contradictory objectives;4 to the damning: that the sector is rife with greenwashing and at risk of a miss-selling scandal,5 or that funds offer little, if any, environmental benefit and cause actual harm by misleading investors into thinking they are addressing climate change when they are not.6

Genuinely low carbon strategies and investing directly in climate solutions (including via private equity) are, of course, an effective way to reduce carbon footprints and to allocate capital to climate change mitigation. They are, however, concentrated in a small number of sectors, thus risking financial underperformance.

US NGO Forest Trends argued in February 2021 that while continued climate policy tightening should create a positive secular trend for low carbon investments, low carbon strategies could become expensive (either because policy is insufficiently ambitious or because flow of funds into low carbon products drives valuations too

high).7

Since then, clean energy indices have underperformed dramatically compared to the traditional energy sector: the MSCI World Energy Index outperformed the MSCI Alternative Energy Index by 59% in 2021 and 43% in the year to 31st August 2022.

Thinking clearly about achieving both financial and low carbon goals

Both investment managers and retail investors need the flexibility to switch out of green assets if they perceive them to be overvalued.

Moreover, the sectors where emissions are hard to abate remain critical to economic growth and the transition to

a carbon neutral economy.

Investments in some carbon-intensive companies represent both an opportunity to finance businesses leading the way to net zero and at the same time achieve superior returns.

In these scenarios investors can hold more carbon intensive portfolios and pay for credits to maintain the same carbon footprint or pay extra to achieve net zero today.

Most investment vehicles are designed to maximise financial returns with no built-in willingness-to-pay for public goods.

These investment vehicles do not lower the cost of capital. Sometimes achieving environmental or other ethical investment goals requires an element of philanthropy, a willingness-to-pay.

This is relevant for the mitigation of climate change, central to which is addressing how the global community funds projects and programs that do not offer commercial returns.

There is growing evidence of consumer appetite to offset the carbon impact of a range of activities from flights to car fuel and credit card purchases.

Private investors can also pay for high integrity carbon credits and thus accept below-commercial returns to have a climate impact that goes beyond business-as-usual.

After all, it will be impossible to stabilise global warming below 2°C without offsets and negative emissions including “Natural Climate Solutions”.8

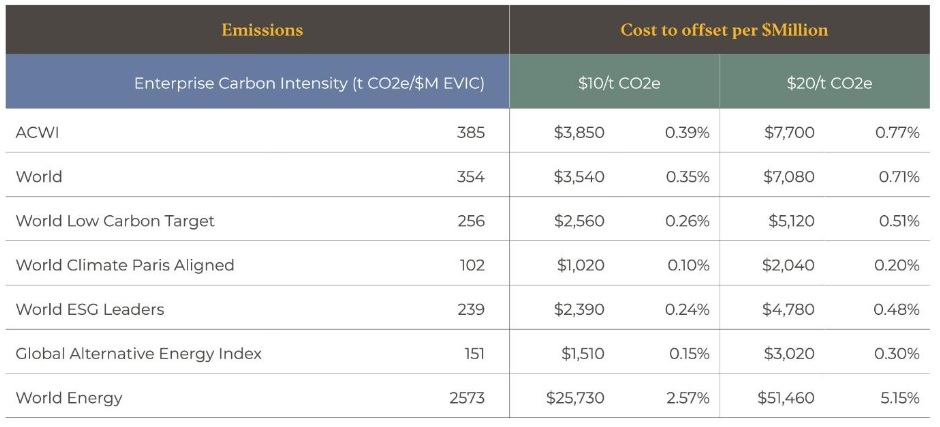

Table 1 below shows the emissions (Scopes 1, 2 and 3) associated with a range of MSCI indices measured as tons of CO2 equivalent per $ million of Enterprise Value including Cash (EVIC), as at the end of August 2022.

At what would currently represent a high carbon credit price of US$20, the leading MSCI ACWI index would cost 0.77% per annum to offset, the Global Alternative Energy Index 0.30% and the World Energy Index a much higher 5.15%.

Table 1: MSCI indexes, carbon intensity and cost to offset as at 31st August 2022

However, as we noted above, the World Energy Index outperformed the Alternative Energy Index by 59% in 2021 and 43% in the year to 31st August 2022, sufficient to pay for offsetting the difference in carbon footprint between the two indices for many years, and still leave profits available for other forms of philanthropy or for risky “impact” investments.

Considerations

Carbon credits can therefore be used both to achieve net zero earlier than 2050 and to optimise the financial performance of carbon constrained investment strategies, representing a more efficient and impactful use of capital if low carbon portfolios are overvalued or if ESG strategies are failing to deliver meaningful climate change

mitigation versus non-ESG benchmarks.

Investors who wish to lower the carbon footprint of their investments should not solely rely on ESG products. Nor do they always need to rely on low carbon funds and indices.

Artorius clients have the advantage of bespoke carbon footprint data for their portfolios provided by Sugi using S&P Trucost analytics. So, they will be able to discuss with their relationship managers how best to make decisions most

appropriate for their goals and risk profiles.

1. https://www.unepfi.org/net-zero-alliance/

2. Financial Sector Science-Based Targets Guidance Version 1.0 February 2022.

3. Financial Sector Science-Based Targets Guidance Version 1.0 February 2022.

4. https://www.ft.com/content/c8b11672-4847-44ae-b132-

788cb2383a2c?shareType=nongift

5. https://on.ft.com/3s3UHUu; https://on.ft.com/3Nu8r3m

6. Tariq Fancy. The Secret Diary of a Sustainable Investor.

7. The Net Zero Transition and Offsetting of Carbon Intensity in Retail Investment Portfolios. Rupert Edwards. Forest Trends.

8. Natural climate solutions are conservation, restoration and improved land management actions that increase carbon storage or avoid greenhouse gas emissions in landscapes and wetlands across the globe.