Is cash really king?

By Gary Asquith, Business Development Manager at BHP Financial Planning Ltd

For many investors, returns from global financial markets have been stagnant over the last few years, albeit share and bond markets had a particularly good run towards the end of 2023.

Meanwhile, cash-based alternatives offered by banks and building societies have grown in popularity due to the current climate of higher interest rates. While it can be tempting to consider switching from an investment portfolio to a savings account, history would tell us it’s unlikely to be the best solution for your long-term financial planning.

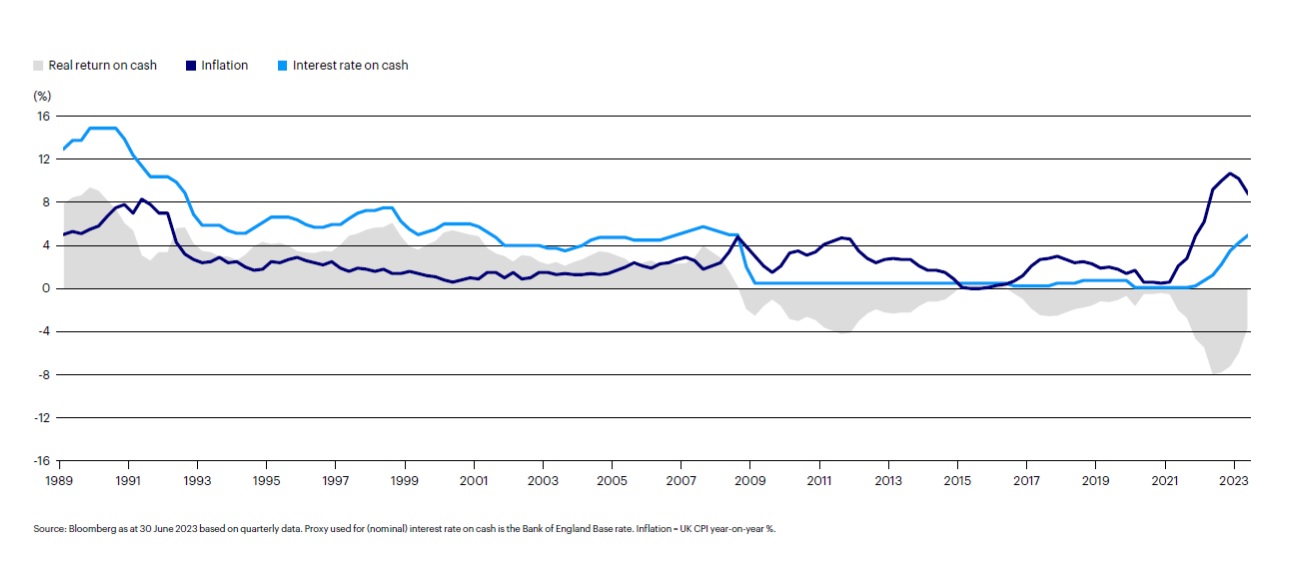

The real return of cash

In 2023, financial institutions continued to increase interest rates available to savers. However, the ‘nominal return’ advertised is not always as attractive as it may initially appear. A key point to consider is your ‘real return’ – in other words, does your money grow once we have taken account of inflation?

The fear of missing out

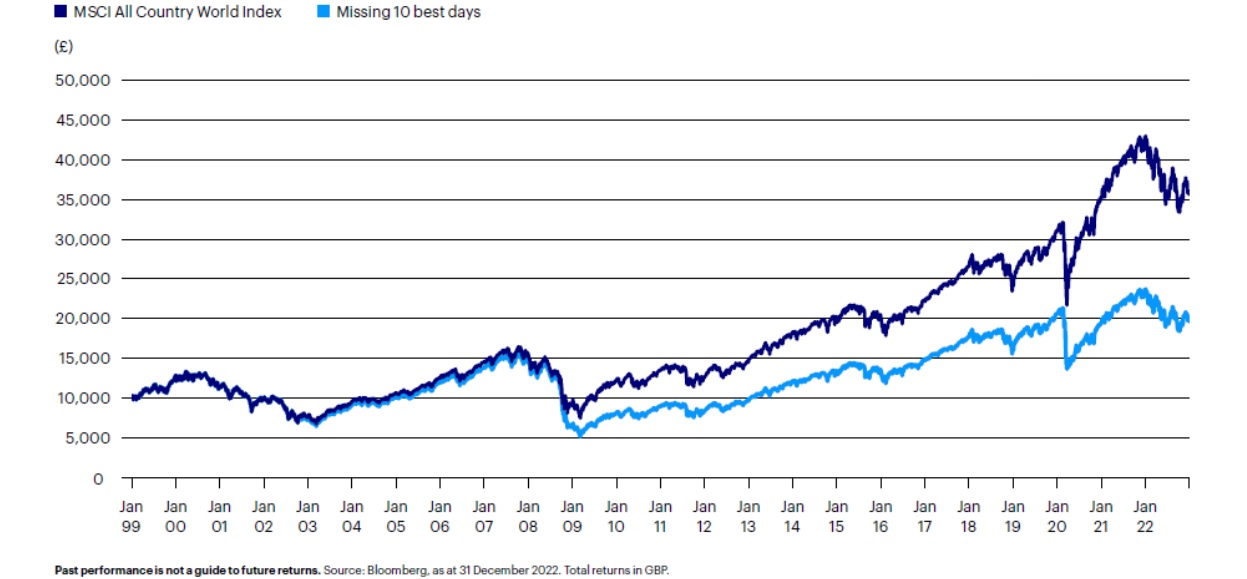

Volatility is a normal part of investing – markets rise and fall in the short term and it’s natural to feel frustrated during periods of stagnation. But we shouldn’t be surprised by them and should resist making reactive decisions that could be harmful.

History highlights that when markets surge, they tend to do so quickly and without warning – for example, who could have predicted that both global stock markets and UK government bonds would deliver a return of around 8% in the last two months of 2023 alone? As long-term investors, it’s important to be on the plane when it takes off, to capture these market returns when they arise and avoid the ‘fear of missing out’.

History highlights that when markets surge, they tend to do so quickly and without warning – for example, who could have predicted that both global stock markets and UK government bonds would deliver a return of around 8% in the last two months of 2023 alone? As long-term investors, it’s important to be on the plane when it takes off, to capture these market returns when they arise and avoid the ‘fear of missing out’.

The importance of staying the course through the good and the bad, however, is paramount to providing a successful investment outcome. At present, cash may appear advantageous, but other factors such as inflation, your tax position and the chance to miss out on the aforementioned strong and unexpected returns, quite often mean that the best solution for your long-term planning is to remain invested.

Other things to consider

Ultimately, when it comes to saving money and planning your finances, cash savings and investments are both important and each have an important role to play.

Savings are ideal for short-term or unexpected expenses such as holidays or the boiler breaking down. But if you’re looking to build your wealth for the future, it’s worth considering investing because stock markets tend to perform better than cash over a greater time period.

If you are planning your finances for the longer term – five years or more – investing offers the opportunity to get your money working harder, because you should get better returns than you could from cash.

But this can’t be guaranteed as stock markets fall as well as rise, so you could get back less than you invest. That’s why a combination of both savings and investments can be a good thing to aim for.

With the complexities involved, it’s always best to speak to a qualified financial adviser to ensure you have peace of mind. And at BHP we’re available to offer advice and guidance on reviewing your investments or cash position. Simply get in touch with me via gary.asquith@bhp.co.uk or call 0333 123 7171.

Please note that the information included in this article is provided for general guidance and information purposes only. It is not intended to amount to professional advice, and you should not use it as a substitute for professional advice tailored to your specific circumstances. We do not accept responsibility for any actions and disclaim liability for any actions you take (or omit to take) based on this article and you should take professional advice based on your specific circumstances before proceeding.

BHP Financial Planning Limited is authorised and regulated by the Financial Conduct Authority.