Securing refinancing in the current debt markets

The debt markets have experienced a tumultuous few years, but the path is smoother now. George Fieldhouse and Chris Sharpe from Grant Thornton explain what the landscape looks like in the middle of 2024 and how companies can navigate a refinancing.

They focus on five key points – the evolution of lender appetite, the lender pool, preparing the right information pack for a refinancing, timing considerations, and the outlook for refinancing in 2024.

They focus on five key points – the evolution of lender appetite, the lender pool, preparing the right information pack for a refinancing, timing considerations, and the outlook for refinancing in 2024.

There’s no getting away from the reality that 2022 and 2023 was a challenging time from a macroeconomic perspective, coming hot on the heels from the turmoil faced throughout the COVID-19 pandemic.

Notwithstanding the deal-boom of the immediate post-pandemic period, economic growth has been anaemic, not helped by global economic headwinds and high-inflation impacting raw materials and energy, as well as payroll and other input costs.

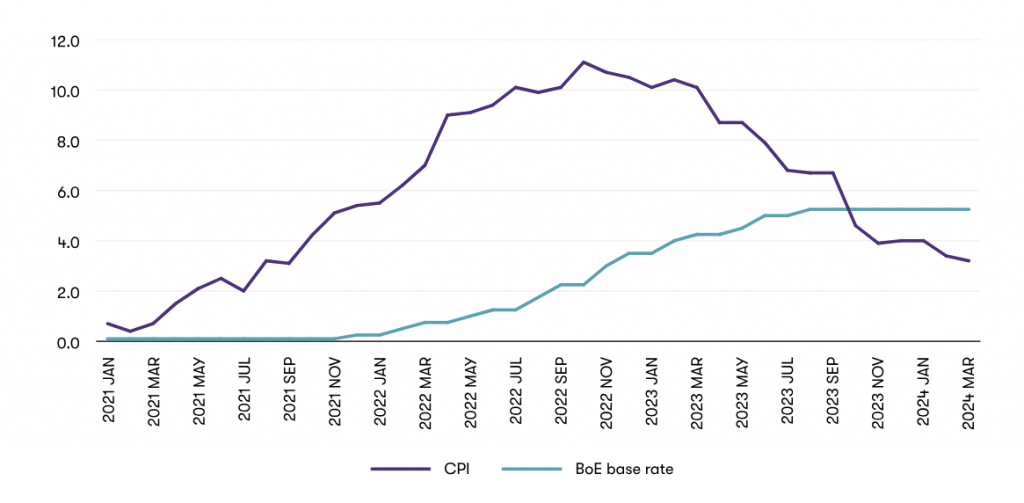

The Bank of England sought to tackle inflation through increasing interest rates to reduce demand, which saw base rate increase from 0.1% in December 2021 to 5.25% in August 2023. The increase in rates took time to filter through to inflation, with CPI rates above 10% between July 2022 and March 2023 and only decreasing to 6.7% by September 2023.

More positive news was received recently, with CPI inflation decreasing more rapidly to 3.2% in the 12 months to March 2024, resulting in the markets starting to price in a reduction in interest rates from around the middle of the year.

Monthly CPI inflation and BoE interest rates (Jan 2022 to Mar-24)

Source: Office for National Statistics

The evolution of lender appetite

From a lender perspective, appetite was already weakening coming into 2022 and softened further with geopolitical and macroeconomic instability. Lenders concerns were focused on demand, inflation, margin sustainability, and profitability.

The limited risk appetite was further eroded in the UK by the 2022 ‘mini-budget’ which brought a tightening of monetary policy to the top of the agenda. So, with concerns over margin and profitability on one hand and interest rates on the other, borrowers were hit with a perfect storm as to debt serviceability.

These concerns were mirrored and amplified in lenders’ credit committees where risk-appetite was materially reduced, resulting in a dramatic decrease in debt financings in H2 2022 and into Q1 2023.

However, from Q2 2023 the UK lending market began to open up. While inflation proved to be more persistent than had been expected, and base rates continued their rise, lenders and borrowers alike became more confident in corporates’ ability to manage or mitigate these pressures and had better evidence to support that view. Interest rates remain a concern, but with the consensus that the direction of travel is favourable, appetite to test the market and lenders’ desire to transact has noticeably increased in 2024.

To further support this development, lenders have significant capital to deploy and, despite the boost to their own income from the higher SONIA rates (notably for the debt funds who largely don’t need to pass on the increased SONIA rates), they need to deploy to earn arrangement fees.

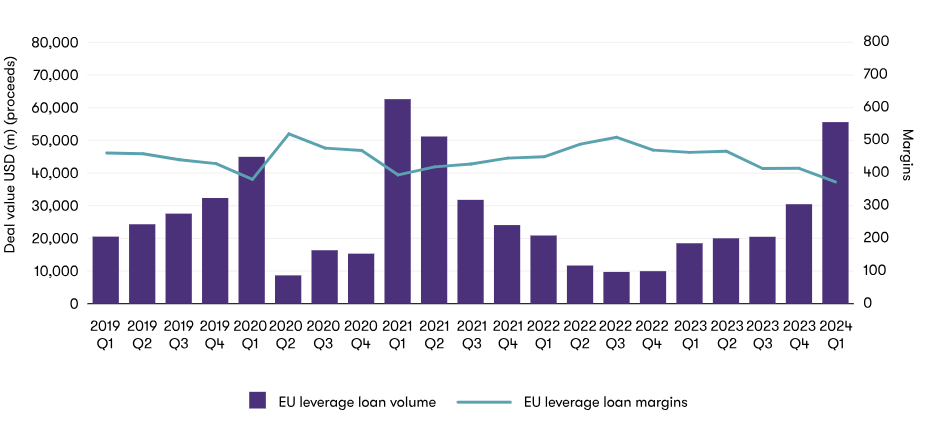

This appetite can be clearly seen in the wider European leverage loan markets, which saw a significant uptick in volumes in Q1 2024 (indeed the highest level of deployment since Q1 2021), and a continued fall in margin on new loan issuance.

European leverage loan volumes and margins (Q1 2019-2024)

Source: Debtwire

In the UK mid-market this increase in wider activity levels has been mirrored in a notable increase in lender appetite, with more lenders providing guidance on terms and a build in competitive tension in financing processes. While we’ve seen improvements in indicated pricing and other terms such as covenants, lenders remain cautious on leverage given the ongoing high (in recent history) base rates.

The expectation is that increased lender appetite, coupled with an overhang of M&A transactions, and refinancings not completed in 2022/2023 will support a sustained uptick in deal volumes throughout the second half of 2024.

Considering the lender pool

With an improving but still challenged debt market, it’s crucial that borrowers approach their financing in a considered manner with a clear view of their objectives and the targeted lender pool, and with supporting materials such as information memorandum, financial model, and due diligence.

Any refinancing will combine a range of objectives, from quantum to pricing and covenants and numerous other factors. Frequently these aspects are interrelated, and so the ranking of objectives with a preferred and fall-back position is important.

Depending on the prioritisation of these objectives there may be differing lenders brought into the mix. Given the current market, borrowers shouldn’t overly limit the pool of available capital and we recommend approaching a broader range of lenders (by number but also by type or category of debt) than may have been the case in previous refinancings. This may include the main senior banks, the challenger banks, debt funds, and non-cashflow based lenders, who may include asset-based lenders focused on receivables, stock, etc, and property or real estate-based lenders.

Preparing the right information pack for a refinancing

Once the financing objectives and pool of lenders has been assessed, preparation of an appropriate information package is crucial. A direct consequence of the more unsettled market has been an increase in lenders’ information requirements, both borrower-prepared and independent diligence or valuations. The extent to which a lender will require third-party due diligence will depend on the specific circumstances.

Where a borrower is already known by the lender and the extent of the new borrowing is relatively limited, due diligence requirements may be minimal. The requirements can be expected to be higher for a new borrower in the current environment, particularly when the business operates in a higher-risk sector and the proposed borrowing results in a significantly leveraged balance sheet and a considerable interest expense.

In such circumstances, a lender is highly likely to require third-party financial due diligence to include a focus on historical financial performance, the achievability of the base case financial projections (and sensitised case) and the serviceability of interest payments. It can be expected that lenders will leverage the third-party financial due diligence to support with setting covenants and the quantum and structure of the lend.

Judging the right level of preparation ahead of a process is important and a delicate balance between under-preparation and losing lenders on one hand and over preparation with consequences for timing and cost. Not all lenders will require the same data set and it may be possible to defer some elements until a process is underway and lender requirements are confirmed.

Timing considerations

When planning a refinancing, a key consideration should be the timing of the audited accounts and the importance of being able to prepare the accounts on a going concern basis without any potentially damaging disclosures.

Management’s going concern assessment needs to consider at least the 12 months from the date when the financial statements are authorised for issue. If there’s uncertainty around the availability of necessary funding during this period, this is likely to require a disclosure. As such, advanced planning is vital, and we typically advise clients to avoid entering into the final 18 months of any financing period without having finalised their future plans.

As well as planning when to commence a refinancing process, borrowers should also be mindful that processes are typically taking longer. This is somewhat linked to the additional information required, but timing is also being extended due to lenders’ credit processes becoming more involved, with greater levels of review and more incidence of pushback on terms that had been negotiated between the lender deal team and the borrower.

Breaking the cycle of Q&A to allow the transaction to move forward is a delicate balance, but as for due diligence, fuller, and well-prepared answers, but also open conversation with the lender as to what they’re looking to achieve is the best route to closing out their requirement.

The outlook for refinancing in 2024

Even as the debt markets open up, challenges still remain – driven by both the difficult economic conditions and associated high interest rates. Borrowers can expect lenders to continue to carefully assess all new lending, resulting in additional information required to support a deal and longer lead times to complete.

In the current market conditions, we’re positive that deals can be successfully concluded, but early dialogue is needed with all parties, including advisers, auditors, sponsors, and potentially a broader range of lenders.

For more insight and guidance, get in touch with George Fieldhouse or Chris Sharpe at Grant Thornton.